CPA Finances Demystified

For those new to the world of municipal finance, it can be a bit difficult to understand the ways your total CPA funds are placed into various accounts and then spent -- but don’t panic! This article aims to demystify CPA finances and help you navigate the murky waters at the intersection of CPA and municipal finance planning and management.

Every year, the Community Preservation Committee (CPC) is required to prepare an annual CPA budget, which is then voted on by the legislative body (Town Meeting or City Council). For most communities, this happens in the spring along the same timetable as the general municipal budget process. The first step in the process is to work with your accounting staff to determine the total amount of CPA revenue the community can expect to receive during the next fiscal year. This total revenue figure should include an estimate of the CPA local surcharge revenue PLUS the estimated matching money to be received in November from the CPA Trust Fund. Once the total revenue has been determined, the annual budget breaks it down into the various CPA accounts.

Breaking Down the Annual CPA Budget

Here are the different CPA accounts that comprise your annual budget...

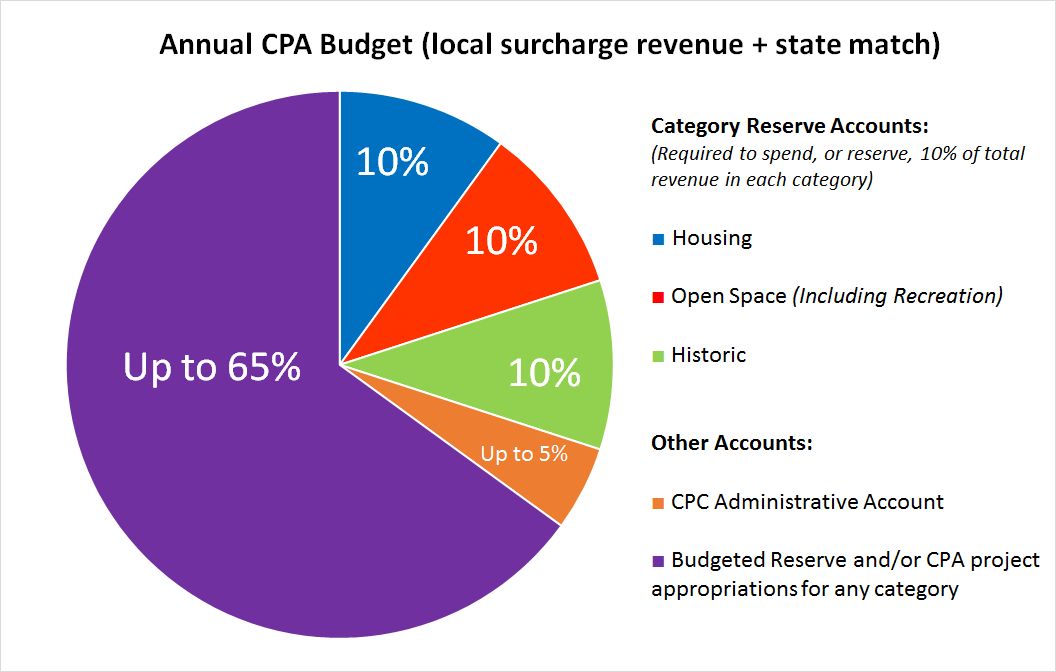

CPA Category Reserve Accounts:

The CPC is required to spend, or set aside for later spending, 10% of annual CPA revenues for each of the main three CPA purposes – Historic Preservation, Open Space (including Recreation), and Community Housing. To create a paper trail proving that this rule was adhered to, the Coalition recommends that these funds are first transferred to the reserve accounts as part of the annual budget and then later appropriated from the reserve accounts for specific projects.

But remember, the rule is "spend or reserve," so you don't have to put 10% in the reserve accounts if you are recommending specific projects that are more than 10% of the annual revenue. However, if the legislative body rejects the project that was supposed to fulfill your 10% requirement, you will be in violation of the rule. So that's why we recommend first transferring the funds to the appropriate category reserve account and appropriating from there.

Any money remaining in a category reserve account at the end of the fiscal year stays in that reserve account until appropriated for a project. Funds in a category reserve account are “restricted” funds, and they can only be used for that specific category. Once funds are transferred to a category reserve, they cannot be transferred out and spent for a different purpose.

CPC Administrative Fund (Up to 5% of Total Annual Revenue):

Each year, your CPC also has the option of requesting that the local legislative body (Town Meeting or City/Town Council) appropriate up to 5% of annual CPA revenues for the CPC’s administrative needs during the fiscal year. The CPC typically has many expenses during the fiscal year, such as hiring administrative staff and paying for due diligence work on proposed CPA projects. Once appropriated, administrative funds can then be spent at the discretion of the CPC during the fiscal year. However, unlike a reserve fund, this account is only available for one fiscal year, and will be closed out automatically by your City or Town Accountant at the end of the fiscal year. Unused funds from this account will be transferred to the CPA Fund Balance account. See below for more information on the fund balance account.

CPA Budgeted Reserve Account:

After the CPC has figured out the amount of your total anticipated revenue that will be used for projects, administrative expenses, and the 10% category reserves, there may be additional anticipated CPA revenue that you don't have an immediate need for. An optional "budgeted reserve" account can included in the CPA budget to temporarily park this money in case you need it for additional projects that arise during the year. If you don't place this money in a budgeted reserve, you will temporarily lose access to the funds when the town sets its tax rate in the fall. Putting the unused money in a budgeted reserve allows the community to access the funds during the entire fiscal year for any CPA purpose, following the normal procedure for CPA recommendation and legislative body vote. At the end of the fiscal year, the unused balance in the budgeted reserve will automatically be closed out by the City or Town Accountant and added to your CPA Fund Balance account. See below for more information on the fund balance account.

What Happens With The CPA Budget After CPC Recommendation?

Once the Community Preservation Committee has decided on a budget for the coming fiscal year, the committee must take a vote to recommend it to the legislative body (City Council or Town Meeting). The CPC should vote after the budget article has been written in the proper format for presentation to the legislative body. Here is a sample budget format that is suggested by the Department of Revenue (provided here as an editable Word document):

Sample CPA Annual Budget Article

After the legislative body votes to approve the CPA budget for the coming fiscal year, the municipal officials will set up the various accounts in their finance system. Any money that was appropriated by the legislative body, typically for the CPC administrative fund and individual CPA projects, will be available for spending once the new fiscal year begins on July 1st. Any money that was reserved by the legislative body, typically in the three category reserves and/or the budgeted reserve, will be available for appropriation on July 1st. However, these funds are sitting in a reserve account and have not been appropriated, so it will take a CPC recommendation and legislative body vote to spend the money on a CPA project.

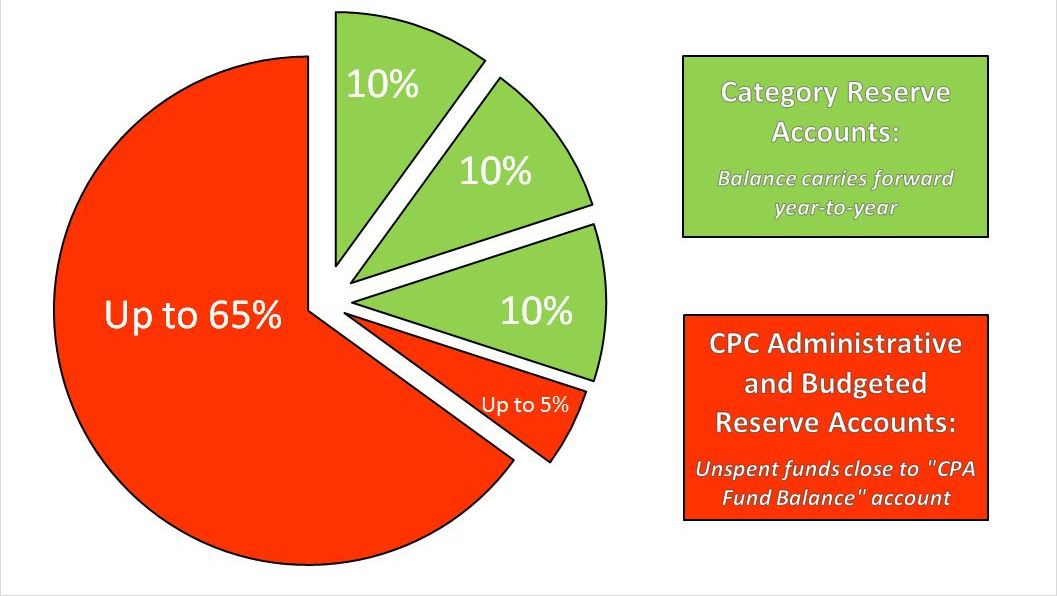

What Happens to CPA Funds At The End of Each Fiscal Year?

CPA Fund Balance:

With the exception of the 10% category reserve accounts, all unappropriated CPA funds are automatically transferred to the "CPA Fund Balance" (sometimes called the "Undesignated CPA Fund Balance") at the end of each fiscal year. This would include funds remaining in your Budgeted Reserve Account, unspent Administrative Funds, interest earned in the CPA accounts, and any other unappropriated CPA revenue. Once the municipality closes its books over the summer, the money in the CPA Fund Balance account is available for appropriation for any type of CPA project.

Here is a look at what happens to each of the CPA Accounts at the end of each fiscal year:

Which Accounts Can Be Used to Fund CPA Projects?

So now that you're familiar with a typical annual CPA budget article, let's move on to appropriating money for specific projects. When recommending projects, it is the job of the CPC to decide on a funding source for each project. It's not good enough for the CPC to say it recommends spending $20,000 to preserve town historic documents. The CPC should also specify which CPA account (perhaps multiple accounts) should be used as the source of funds for that $20,000.

Here are the various accounts that you can use to fund specific CPA project recommendations:

- CPA Category Reserve accounts (Historic Preservation, Open Space (including Recreation) or Community Housing)

- CPA Budgeted Reserve account from the current fiscal year

- CPA Undesignated Fund Balance (money left over from previous years)

- Annual Fund Revenues (the estimated CPA revenue for the upcoming fiscal year. These funds cannot be spent until July 1st)

- Borrowing (issuing a bond to be paid from the future CPA revenue stream)

Want to take an even deeper dive into these five possible funding sources? Click here for a useful chart with further details.

A Handy Strategy for CPA Fund Management:

To give your community the maximum flexibility with its CPA spending, it’s always wise to spend the most restricted CPA funds first. So, if you have a project recommendation to make, always recommend that funds be pulled from the appropriate CPA Reserve Account first. For example, let’s say you are recommending a $50,000 project to preserve historic town documents. You know that there is $10,000 in your CPA Historic Reserve fund and $300,000 in your CPA Undesignated Fund Balance. While you could pay for the entire project from your CPA Undesignated Fund balance, you’ll want to recommend that the project be funded with $10,000 from the Historic Reserve Account and $40,000 from the CPA Undesignated Fund Balance. By spending the restricted funds first, you will have more "undesignated" money that can be spent on projects in any category.

Perhaps your CPC has developed some other strategies it uses to make CPA budgeting and project recommendations easier? If so, please let us know, so we can share these with other CPA communities. And remember, if you’re stuck and need help during budget season, don’t hesitate to give us a call at 617-367-8998. We’re here to help!

Feb. 2018