Has Your Housing Trust Spent CPA Funds? Make Sure They Report Back to the CPC!

With each passing year, more communities establish Municipal Affordable Housing Trusts (MAHT's) in order to address local housing needs, and CPA has become an increasingly popular funding source for these local trusts. But if your community grants any CPA funding to your local MAHT, it's vital that the trust reports back to the CPC on how they've spent those funds!

With each passing year, more communities establish Municipal Affordable Housing Trusts (MAHT's) in order to address local housing needs, and CPA has become an increasingly popular funding source for these local trusts. But if your community grants any CPA funding to your local MAHT, it's vital that the trust reports back to the CPC on how they've spent those funds!

In 2016, Governor Baker signed into law a municipal government reform package that included changes in how CPA funds are transferred and used by MAHT's. There are two important pieces to this law that CPC's should be aware of:

- All CPA funds that are transferred to a Municipal Affordable Housing Trust need to be accounted for separately from other trust funds. Each CPC should make sure that the person doing the financial work for the Trust understands this requirement.

- All MAHTs that spend CPA funds must report their expenditures annually to the local Community Preservation Committee. The CPC, in turn, must then enter the trust expenditures in the state's online Community Preservation Projects Report, Form CP-3.

How should Municipal Affordable Housing Trusts report these CPA expenditures to the CPC?

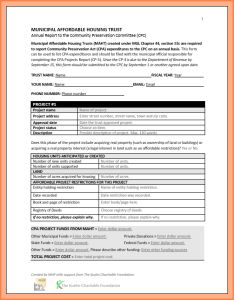

To assist trusts in reporting to the CPC, the Mass Housing Partnership worked with the Coalition to create a fillable MAHT CPA expenditure report that outlines the information that needs to be entered into the Community Preservation Projects Report (CP-3). Since the CP-3 report is due to the Department of Revenue on September 15th each year, it's recommended that trusts submit their reports to the CPC by September 1 or another agreed upon date.

To assist trusts in reporting to the CPC, the Mass Housing Partnership worked with the Coalition to create a fillable MAHT CPA expenditure report that outlines the information that needs to be entered into the Community Preservation Projects Report (CP-3). Since the CP-3 report is due to the Department of Revenue on September 15th each year, it's recommended that trusts submit their reports to the CPC by September 1 or another agreed upon date.

- Download the CPA Expenditure Report Form for your Municipal Affordable Housing Trust

- Download the Reporting Instructions for your MAHT

Be sure to keep in mind the following tips when collecting this CPA expenditure information from your local trust:

- CPA expenses for each project undertaken by the trust should be reported on separately - make sure your trust fills out a separate form for each CPA expenditure.

- If the trust had permission to use CPA funds for administrative expenses, the total of those expenses should be reported as one "project" each year.

- When your community initially approves of a grant of CPA funding to your local MAHT, this gets reported in the CP-3 as an appropriation "To a Fund/Trust" under the Project Type section. In order to avoid having these CPA funds counted twice in your reporting, each MAHT expenditure must then be entered separately as a new project, and "From a Fund/Trust" should be designated as the source of funds in the Funding section. For more details, reference the CP-3 Instruction Manual.

If you have any questions on the CP-3 reporting process, the Coalition is always happy to help. Feel free to give us a call at 617-367-8998 if you need any assistance.

Feb. 2022